Food crises

Download Food crises.pdf

Food crises:

A consequence of disastrous economic policies

A brief historical reminder

For as long as one can remember, agriculture has been subject to crises that often translated themselves into famines. Since early antiquity, literature is full of references to famines. During the Middle Ages, Europe faced a series of such events, and the famines that preceded the French Revolution of 1789 and the Russian Revolution of 1917 have often been presented as one if not the main factor of the popular upheavals that triggered them. These famines occurred in relatively closed economies where commercial exchanges were limited. They were essentially crises due to an absolute lack of availability of food and can be defined as supply crises.

Modern crises, such as the Bengal crisis of 1943 that was brilliantly analysed by Amartya Sen, or the international food crisis that occurred during the 70s, the 2007-2008 food security crisis and the period that we are currently experiencing (2012) are of a very different nature. They generally are not crises due to food shortages, as global food availability is largely sufficient to feed each and everyone, and the infrastructure is in place to bring commodities to the areas where there may be a localised shortage. Rather, they are food access crises for a mass of people who live in poverty and do not have enough resources to purchase the food they need. Modern crises are also increasingly, particularly since 1970, global in scale while historically crises were more local.

The food crises of the mid 70s and of 2007-2008 both followed a period of great agricultural market stability that was characterised in the first case by a strong increase of world production, and in the second by a decreasing trend in food prices. The 50s and 60s had experienced a steep increase in production (+80%) due to a remarkable growth in productivity and in the area cultivated, as well as to the large-scale use of new high yielding varieties and chemical agricultural inputs (green revolution). In 2000, agricultural prices hit a historical low while international trade volumes had grown exponentially.

These two crises had both started with situations of drought. In the case of the crisis of the 70s this resulted in a reduction in world food production - attributed at the time by some experts to climatic change. However, 2008 was a record production year despite drought in Australia and Canada.

Both crises also coincided with rapid rises in energy prices with important consequences on the cost of food production and transport. In 1973, the price of oil quadrupled, and it tripled between 2003 and 2008.

Both food crises occurred at times when global food stocks were very low. This created a price surge (see box on price volatility). In 1974, cereal stocks were equivalent to 26 days of consumption, while in 2008 stocks represented only 20% of yearly consumption, a dramatic fall when compared to 2000 when their level was of about 35% of yearly consumption.

Finally, in both cases, some food exporting countries decided to impose restrictions on their exports with the aim of protecting their consumers. This created panic on international markets. So much for the similarities between the two crises.

The food crisis of 2007-2008: a policy story

What characterises the 2007-2008 crisis is that it followed a period during which agriculture was largely abandoned by many governments because of a generalised change in the development strategies adopted by most countries. World prices had decreased steadily in real terms between 1980 and 2000, and investment in agriculture had been neglected. At the same time, the dynamic growth of emerging countries such as Brazil, China and India, meant that world food demand was growing rapidly. In non-industrial countries, the ease of access to international aid in case of food emergencies had encouraged governments to direct their scarce resources towards sectors other than agriculture.

During the first part of the first decade of the XXIst century the links between agricultural and energy markets were tightened because of the progressive emergence of agrofuels made from crops. Agrofuels constitute a new form of demand for agricultural commodities that has expanded in recent years, additional to the demands for human food and for livestock feeds. Agrofuels benefit from considerable subsidies (more than USD 10 billion per year). From this perspective, the 2007-2008 food crisis may be considered as a demand-driven crisis, in the sense that a new level had been reached in demand for agricultural commodities because of the emergence of agrofuels. To support this statement, it is worth mentioning that out of a total of 40 million additional tonnes of demand for maize in 2007/08, almost 30 million tonnes were absorbed by ethanol plants in the US. It is this structural change that makes some experts believe that the price increases observed in 2007-2008 will be long-lasting.

Economic conditions at the time of the crisis - weak dollar, low interest rates and burgeoning financial markets increasingly interested in agricultural commodities - added more pressure on agricultural prices, although the extent of their real impact, particularly that of financial speculation, remains a controversial subject. Experts agree that the scale of financial resources engaged in speculation on food commodities is small compared to those committed to energy or metal markets, and the link between these moneys and the increase of prices has not been established in an absolutely conclusive way. Two opposing points of view have been adopted by experts. Some consider that non-commercial market operators have been attracted by prices that were increasing for other reasons (point of view of, among others, the IMF). Others believe that financial speculation is a cause of the price increase.

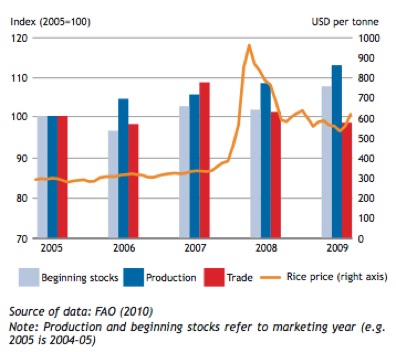

The case of rice, in 2008, is worth analysing in more detail, as it illustrates how price surges can be created by policies implemented at country level. The price of rice increased threefold in a matter of a few months in 2007-2008 although rice production had reached record levels (see diagram) and stocks were at levels comparable to what they had been in previous years. It is probable that it was pressure on other markets (soybean, maize and wheat) that created a panic-driven movement which caused some countries to limit or ban rice exports, while others made precautionary purchases on the world market; all of this occurred without any consultation be it regional (in Asia in particular) or international, for fear that tensions from other commodity markets would be transmitted to the rice market.

Evolution of prices, production, international trade and stocks of rice (2005-2009)

Source: The 2007-08 Rice Price Crisis, FAO 2011

The 2007-2008 global food crisis was therefore largely a consequence of policies implemented by countries at national level:

-Policies of neglect of agriculture by industrial as well as non-industrial countries

-Subsidies on the production of agrofuels in industrial countries (more than USD 10 billion per year in the US and the European Union)

-Macroeconomic policies that have resulted in a weak US dollar and low interest rates

-Insufficient regulation of financial markets

-Limitation or ban of exports and public purchases of food commodities on the world market.

It is interesting to note that the 2007-2008 crisis has had strong implications on the nature food and agricultural policies implemented by countries (see FAO’s FAPDA initiative, its tool and its publications of 2009 and 2012) as it induced countries to reconsider their food and agricultural strategies.

Price increases in 2010-2011: another policy story

The price increase experienced in 2010-2011 is also in part a result of policies, although of a different nature. The drop in prices observed after the peak of 2007-2008 was largely put down to the financial and economic crisis that led to a serious drop in world demand including in emerging countries. It is, however, important to note here that agriculture resisted the effects of the economic crisis rather better than other sectors.

The economic upturn observed at the end of 2009, followed by the strong upturn in the BRIIC countries (Brazil, Russia, India, Indonesia and China) revived demand and international trade of agricultural commodities, bringing again some tension on the world markets. This tension occurred mainly on the sugar, wheat and maize markets, but not on the rice market which had been most hit in 2008. This can be explained by climatic events of 2010 such as drought in Russia, Argentina, Northern China and in CIS countries, followed by floods in Australia which had a tremendous impact on sugar production in that country, as well as with below average yields in Europe, the US and Canada. But rice was not affected by these events and harvests were good and even excellent in some countries (record level harvests were achieved in Cambodia for example).

Even if the general FAO food price index reached a higher level than during the 2008 peak, the cereal index remained below its level at that time. In the short term, evolution of prices depends on estimates of acreage sown and yields estimates. In the medium term, it depends on actual harvests later in the year. Several observers noted a tendency to hold back stocks in order to speculate on future price increases that will contribute to keeping prices at a high level.

The good harvests of 2010 in traditional cereal-importing countries also explain why domestic prices have generally not followed the surge observed on international markets. One possible explanation - which would need to be checked - is that, in addition to the reduction of import tariffs which were widely used in 2008, some countries have taken other measures that are unfortunately poorly documented such as signing of bilateral trade agreements with neighbouring food-exporting countries in order to secure supplies at prices that do not reflect the erratic movements of world prices.

Such arrangements could explain in part the observed limited price transmission of world market prices to domestic market prices. In some documented cases, these agreements have involved bartering gas for wheat, as in September 2008 between Ukraine and Egypt who is the largest importer of wheat in the world. In other countries, like Indonesia, the increase of food prices preceded movements on the world market and was felt as early as 2009. This increase, including for rice, is mainly a consequence of policies aiming at stimulating private consumption as a means to end the economic crisis of 2008-2009.

The analysis of the case of wheat in 2011 helps to better understand the underlying causes and particularly the impact of policies. Reforms of the US agricultural policy and adjustments in the Common Agricultural Policy of the EU have led to a reduction of incentives given to wheat producers in those two economic giants. In the US, wheat production was reduced while maize production increased, as it was more profitable for farmers. This meant that there was a change in the centre of gravity of wheat production worldwide, which moved towards Ukraine, Russia and Kazakhstan (the so-called ‘‘Black Sea’’ zone). These countries, however, experience yield variations twice as large as those in the US or the EU, because of their specific agroclimatic conditions. This meant that this zone represented around 30% of world production of wheat, and this change of location of wheat production automatically induced more variability in the total quantity traded in the world, and therefore more volatility in wheat prices.

To sum up, policies of importance in 2010-2011 are:

-Limitation or ban of exports, particularly in Russia and Ukraine

-Relative reduction of incentives for the production of wheat in the EU and the US

-Policies to stimulate consumption following the economic crisis of 2008-2009

-Monetary policies which keep the US dollar weak and interest rates low

-Lack of progress in regulation of financial markets

-Large public purchases of food products on the world market.

Vulnerability of countries to price increases

There is one issue that remains pending on which there is little information: the real importance of the observed world price in determining prices in importing countries.

Some studies, of essentially a statistical nature, have demonstrated that world prices are variably transmitted to domestic markets, depending on the country. For example, world rice price increases between end 2003 and end 2007 were well transmitted to domestic markets in China and Thailand, but very poorly in The Philippines and India.

The explanation generally given is that countries where transmission is poor have put in place price policy stabilisation measures or have changed their trade policy instruments (e.g. tariffs) to absorb the variation. Another likely cause, but one which is not well documented, could be that some countries have signed bilateral trade agreements with exporting countries which allow them to be supplied with food commodities at stable prices that are independent of world prices. Some bilateral agreements have also made provision for exchange (barter) between food and other commodities or equipment. This type of agreement carries the potential to reduce vulnerability of countries to the fluctuation of world prices.

A recent FAO study (end 2012) shows that there are great differences in prices among regions and between regional prices and world prices (see graph below).

Source: Demeke et al., FAO 2012

Another FAO study shows a considerable variability in the import price of maize in ten African countries that import their white maize mainly from the regional market. It also provides evidence of the limited transmission of this price to producers.

Unfortunately, it is impossible at this point in time to know what the actual importance of this type of agreements is and what proportion of international trade does not take place on the basis of the world price. A study on this topic appears essential to better identify those countries that are more vulnerable to the increase of world prices.

In any case, figures and studies available suggest caution in generalising at the country level price variations observed at the global level.

Lessons learned from the crises of the decade 2000-2010: an error with dramatic consequences

Price volatility came suddenly to the forefront of the agenda by mid 2009, at the time when all analyses showed the central importance of food price increases in international discussions on hunger. Why did this change occur? And is this change a positive move in the fight against hunger and the prevention of future crises?

It is in the declaration that followed the World Food Summit of 2009 that suddenly price volatility became central to the international debate. This was the result of last-minute pressure by industrialised countries, particularly OECD member countries Indeed, none of the documents drafted in preparation for the Summit had mentioned the issue but instead rather stressed the critical role of investment in the fight against hunger. It is hard not to interpret this change of focus to a political manoeuvre aimed at diverting attention away from the lack of respect of commitments made by rich countries during the High Level Conference of 2008 to finance agriculture, and putting forward the importance of market information and regulation. This happened at the time when the financial and then economic crises had become the most important concern of industrial countries. This change of tone was later confirmed and supported by the FAO/OECD Agricultural Outlook report of 2010 and subsequently by the background report prepared by a consortium of agencies under the leadership of the OECD and FAO for the G20 meeting of 2011, organised in France. Paradoxically, although the FAO/OECD report of 2010 focused mainly on price volatility, it emphasised that there were few or no proofs that price volatility of international agricultural prices had increased!. Other well respected experts and UNCTAD also stressed that the recent increase in price volatility did not constitute a change in the decreasing historic trend of price volatility observed during the two last decades... Other more recent studies, especially in FAO, insist on the fact that the increase of volatility observed on global markets (Chicago, etc.) and linked to global financial speculation should not be mistaken with national level volatility which is observed on markets that are often disconnected from the world market for a number of reasons that have already been briefly discussed here. The already mentioned FAO study by Demeke et al. (2012) shows that price volatility in African countries was actually higher than volatility observed on the world market from which these markets are quite disconnected. Other experts admit that it is possible with the data available and depending on the analytical techniques used to give proof for the same period of the increase, the stability or the reduction of volatility of world agricultural prices.

The lack of agreement would not be a serious matter of concern if volatility had not become the current catchword and if the attention of so many people -researchers, experts, decisions makers both national and international was not so fully concentrated on this issue, which appears to be overblown. The central place given to volatility has implications on policies being implemented at all levels. For example, in certain countries of the South, resources allocated to agricultural investment and to infrastructure have been reduced to fund agricultural stock holding and measures of market stabilisation, as well as to increase public intervention in agricultural markets. The international community, in the wake of the 2011 G20 meeting, did not respect its financial commitment of 2008 to fund agricultural investments even though falling investments had been identified in 2008 as one of the main reasons for the food crisis. It has now turned its attention to the establishment of market information systems and has shown some reservations about regulating markets, particularly financial markets, on which there has unfortunately been little action.

One can therefore wonder whether the importance given to price volatility is really justified in the context of the overall objective of reducing hunger in the world. It certainly seems to have been counterproductive and what has gone on in Africa would suggest that the increasing weight given to price considerations is not a top priority in the fight against hunger. Instead, the key issue that Africa is facing is that of inequitable growth. During the first decade of this century, average income per inhabitant increased by 5% in Africa during the decade, but the number of hungry in the continent rose by 30 million. This is a fact that should be a source of fundamental questioning of what has happened, but no one seems to discuss this or even show any interest in it. Instead of focussing so much attention on price volatility, the highest priority must be assigned to putting in place policies to provide social protection for the poorer categories in order to allow them to eat sufficiently and thereby increase their capacity to benefit from and seize economic opportunities created by growth.

This does not mean that there should be no effort to try and stabilise prices and reduce risk in agriculture so as to promote investment in the sector and thus increase food and agricultural production. But let’s not mix up the issues of fighting hunger now and that of increasing agricultural production to face future growth of food demand. We must remember that modern food crises are no more crises due to a lack of availability, but crises due to a lack of access. This does not preclude being concerned about the required increase of food production in the future. World population continues to grow and its standard of living will continue to improve. To face this challenge, there will be a need to invest in agriculture, a sustainable agriculture that instead of contributing further to climate change and environmental degradation will help to mitigate it. Inappropriate policies adopted by countries, whether rich or poor, will have to be challenged: stop subsidies to agrofuels which are competing with food production; regulate food markets and financial flows so that they do not engage in speculation; manage market development in a longer term perspective where the bulk of operations will be handled by a better regulated and more competitive market.

The current biased debate will need to be challenged:

-

• Rich countries cannot escape their responsibility by confusing price increase with price volatility so as to avoid contributing financially to the development of world agriculture, and by pretending that regulation will be sufficient to solve the problem.

-

•While preserving life-saving food aid, there will be a need to give the lion’s share of financial assistance to the support to agricultural development and to social protection

It is only once these principles have been adopted that it will be possible to say that there is a real will to prevent future food crises.

(December 2012)

Annex: Comparing the crisis of the 70s, of 2007-2008 and the 2010-2011 situation

Also read:

Last update: June 2022

For your comments and reactions: hungerexpl@gmail.com