News

8 March 2014

The large multinational corporations in charge of our agri-food system...: upstream corporations

We know that the global agri-food system is ailing: at least one billion undernourished persons, 2 billion people suffering from nutrient deficiencies and around 1.5 billion of overweight or obese persons. In a nutshell, the two-thirds of world population are malnourished.

But do we also know that this system is in the hand of a small group of huge companies that control it, influence production and consumption in order to make huge profits?

It is a fact that, in general - all sectors included -, the world economy is increasingly in the hands of huge multinationals. According to UNCTAD, there were around 4,000 multinationals in 1969. In 2009, they were 82,000 with about 690,000 branches throughout the world. Their turnover has been growing at around 10% per annum since the beginning of the 90s, and in 2010, their economic weight was equivalent to at least 25% of world GDP, USD16,000 billion (more than total GDP of the US) and were responsible for the two-thirds of international trade. Among the 100 largest multinationals, of which 93 have their headquarters in rich countries, there are 9 agri-food corporations. But the real influence of multinationals goes far beyond these figures, as these corporations also control a myriad of firms through contracts, a way which allows them to be in charge at low risk and without having to commit any capital. In 2010, for example, these contracts, concluded mostly with firms in countries of the «South», were estimated to be of USD 2,000 billion in the shape of industrial subcontracting and outsourcing of services, contractual agriculture, franchising, licensing, management contracts and other contractual relationships.

A report by ETCGroup (monitoring power - tracking technology - strengthening diversity), dated septembre 2013) illustrates well the degree of domination of the market large agrochemical companies have been able to achieve in the field of agricultural inputs, all the more as they have been able to organise themselves in huge cartels (Putting the Cartel before the Horse ...and Farm, Seeds, Soil, Peasants, etc. Who Will Control Agricultural Inputs, 2013?). The report shows that in all the sectors but fertiliser, four companies alone weigh more than half of the turn over.

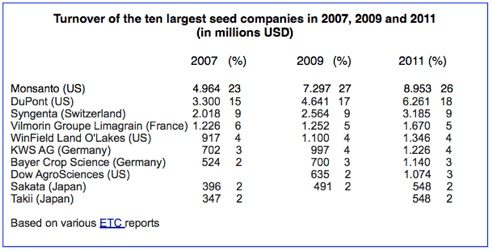

In the seed sector, concentration is very high: 3 companies (Monsanto, DuPont et Syngenta) control 53% of a market of 35 billion dollars, as can be seen from the box below. The business of these companies continues to grow strongly from year to year, in particular through acquisition of local companies in countries in the South, mainly India and Africa, partnerships for developing new varieties, pressure exerted on governments to obtain a strict compliance with intellectual property right rules (in particular through the New Alliance for Food Security and Nutrition) and ‘‘education’’ campaigns for producers.

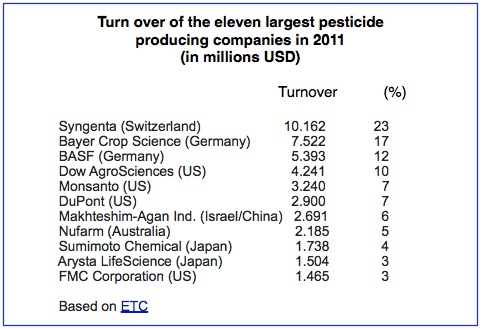

In the pesticide sector, many of the same corporations can be found. All in all, the ten largest multinationals weigh 95% of the turnover of the sector (98% if you add the 11th largest). (See box)

It is estimated that in 2011 the pesticide market grew by 15% to reach around USD 44 billion. The recent trend has been for these corporations to invest in biological pesticide (using bugs and microorganisms) particularly in the case of fruit and vegetables where very few GMOs have been developed so far. This is an important niche that should be growing in the future as it will also help these companies to improve their image with the public.

Few large scale studies have been conducted so far to estimate the cost of using pesticides in terms of number of days of work lost, cost of medical treatment and hospitalisation. UNEP however conducted a study on 37 sub-Saharan African countries which estimates this cost at USD 4.4 billion in 2005, cost of lost lives and the impact on the environment - e.g. destruction of bee populations - not included. This amount represents around 4% of total agricultural production of sub-Saharan Africa (52 countries).

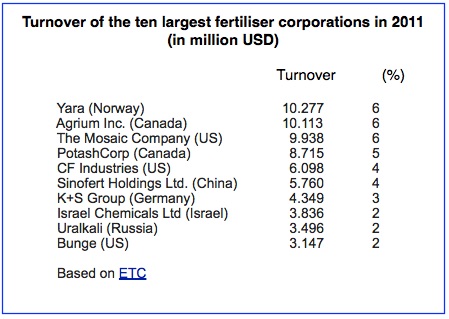

As for the fertiliser sector, it is certainly the one where concentration is less as the ten largest companies ‘‘only’’ represent 41% of sectoral turnover. (see box)

Growth of the fertiliser market, although slower than for seeds and pesticide, is estimated at more than 7% in 2011, when turnover reached USD160 billion, equivalent to about 7% of world agricultural GDP. This is important to notice when considering that this growth occurred despite a strong increase in fertiliser prices in 2007-2008, an increase much higher than for agricultural outputs.

In the case of animal health products, there is again a stronger concentration: the ten largest companies weigh more than 80% of the sector and the total turnover is around USD 22 billion. (see box)

As can be seen from all these data, the agricultural inputs market is not a competitive market. Unfortunately, there is not study that evaluates all the consequences of this highly concentrated market structure. One can however expect that profits made from their business by these giant companies operating in non competitive sectors must be very high and that the prices paid by farmers for these agricultural inputs must be much above what their cost of production and a ‘‘reasonable profit’’ would justify. For what concerns the real cost of using these products in terms of health and environmental degradation, it is likely, as suggested by the very partial study of UNEP in sub-Saharan Africa, to be much higher than the price paid for them, even though these prices are inflated because agrochemical companies adopt a cartel behaviour.

This points to the absolute need for serious studies to be undertaken soonest to estimate the cost of this system and of the use of all these inputs as exhaustively as possible and in a way that makes their results unquestionable. This is indispensable for internalising these costs in the final price of these products. This internalisation of costs could be performed progressively - to allow the system to adapt little by little - by a tax that would have the triple advantage of:

-

•Mobilising resources that could be used among other things to finance public research for developing sustainable agricultural technologies that would be more accessible for poor farmers [read more on this idea]

-

•Reducing the use of agrochemicals

-

•Make agricultural products coming from low-input agriculture (agroecological agriculture, organic agriculture) more attractive for consumers than what they are today when they are more expensive than those produced by conventional chemical agriculture.

The High Level Panel of Experts of the Committee on World Food Security (CFS) should have a central role to play in this extremely important task that would contribute to fix our ailing world agri-food system.

It is quite likely that this will not be easy and that the lobbys supporting the agrochemical industry will do everything in their power for this type of really independent studies never to be conducted.

(To come soon: the food industry multinationals)

-----------

To know more:

-

-Read this other ETCGroup report: Who Will Control the Green Economy? Novembre 2011

Last update: March 2014

For your comments and reactions: hungerexpl@gmail.com